MARKET ANALYSIS OF THE INDUSTRY

Component of the global energy demand – oil remains dominant for a long time

According to the statistics released by BP ENERGY OUTLOOK in 2019, the demand for oil and gas accounts for over 53%, remaining to be the highest proportion, of the global energy demand structure by 2040. Among them, the annual growth rate of gas is 1.7% and its demand exceeds coal as the second largest source of energy of the world. By 2040, oil remains to be the primary component of all kinds of energy, with demand ranging from 80 million to 130 million barrels per day.

Component of global energy demand

In 2018, notwithstanding the fluctuation in crude oil price, oil price gradually recovered over the fluctuation in the first half. The Brent crude oil price gradually increased from US$66.57/barrel at the beginning of January 2018 to US$86.29/ barrel in early October, representing an increase of 29.6%. The Brent crude oil price recorded a sharp decline since October due to factors such as the increased geopolitical risk in the Middle East and the US-China trade war, and the price decreased by 32% to the lowest of US$58.71/barrel by the end of November. In December, oil price basically maintained around US$60. The average annual Brent crude oil price was US$43.74, US$54.15 and US$71.4 in 2016, 2017 and 2018, demonstrating an overall recovery of oil price in the past three years. The International Energy Agency (“IEA”) expects that the supply of global oil will be further tightened in 2019. The IEA expects that the growth in global oil demand maintained at 1.40 million barrels per day in 2019. The overall oil and gas industry was positive.

Increasing Upstream Expenditure on the Oil Industry

According to the statistics of Wood Mackenzie, the capital investment in upstream E&P (Exploration & Production) of the global oil and gas industry has increased and is expected to maintain steady growth during the period from 2020 to 2030. According to statistics of Barclays Bank lc, the capital investment in global upstream E&P increased by 8% from US$357 billion in 2017 to US$383.8 billion in 2018, and is expected to increase by 8% to US$414.5 billion in 2019. Meanwhile, the capital expenditure from global offshore oil experienced a significant increase, and the three largest oil companies in China declared in 2019 that they would increase upstream capital expenditure to improve the overall utilisation rate of rigs.

The Middle East is the most active area in the world for using the jack-up rigs, with utilisation rate and the number of rigs in operation much higher than other regions. According to the 2018 statistics of CLARKSONS, the hotspots of major demand for global shallow water jack-up rigs concentrated in the Middle East, Asia Pacific region, Gulf of Mexico and North Sea of Norway. In 2018, the largest demand for jack-up rigs came from the Middle East, in which 142 rigs in operation with utilisation rate of 77%. The number of rigs in operation and utilisation rate ranked first in the world; the second was the Asia-Pacific region with 68 rigs in operation and utilisation rate of 59% and the third was the Gulf of Mexico with 35 rigs in operation and utilisation rate of 56%.

The number of jack-up rigs in operation and utilisation rate of rigs in different regions of the world

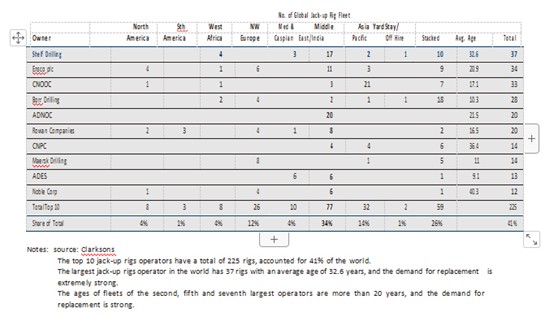

The top 10 operators in the world had received a substantial number of market orders, and their rigs are aging seriously with strong demand for replacement. According to the 2018 statistics of CLARKSONS, the top 10 jack-up rigs operators in the world had 41% of rig assets in 2018, and their average utilisation rate of rigs was 75%, which was higher than the global average of 70%, and their number of jack-up rigs operating in hotspots was much higher than other operators. For example, the number of rigs operating in North Sea of Norway, Middle East, the Asia Pacific region and the Gulf of Mexico accounted for 79%, 51%, 46% and 38%, respectively.

Introduction of major jack-up rig operators:

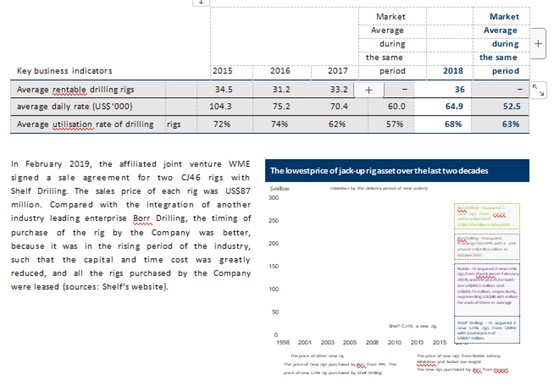

Shelf Drilling: the largest jack-up drilling rig operator in the world with business covering the Middle East, Southeast Asia, India, West Africa and the Mediterranean region. The fleet currently has 37 jack-up rigs. In February 2019, the affiliated joint venture WME signed a sale agreement with Shelf Drilling, and will purchase shares in Shelf Drilling. This business cooperation and integration has expanded the scale of Offshore Assets of CMIC and strengthened the cooperation and future business synergy between CMIC and the global top offshore rig operators.

COSL: a subsidiary of CNOOC and the largest offshore oil field service company. It has 33 jack-up drilling rigs, two of which use the drilling package of TSC brand under CMIC. As a supplier of equipment, TSC, the Company’s brand, has many years of business connection with COSL.

CPOE: a subsidiary of CNPC and the second largest offshore oil field service company. It has 14 jack-up drilling rigs. As a supplier of equipment, TSC, the Company’s brand, has many years of business connection with CPOE.

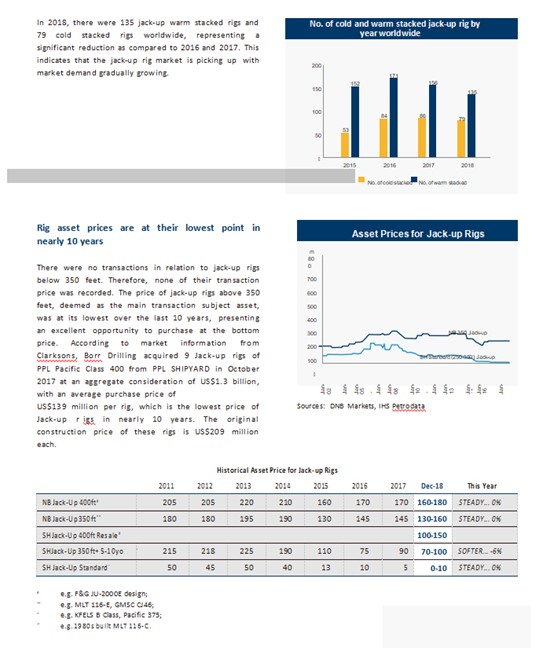

Borr Drilling: the fourth largest jack-up drilling rig operator in the world. Established in 2016, in the past two years, Borr Drilling was an offshore drilling rig operator that have rapidly developed through the acquisition of high specification drilling rigs during the downturn of the industry. It currently has 28 jack-up drilling rigs. Borr Drilling purchased 9 PPL Pacific Class 400 jack-up drilling rigs from PPL SHIPYARD in October 2017, at a total consideration of US$1.3 billion, with an average purchase price per unit of US$139 million. The original construction cost of these rigs was US$209 million.

ADNOC: Abu Dhabi National Oil Company, the 12th largest oil company in the world, and an affiliated joint venture under CMIC. It had two CJ46 jack-up rigs (namely “SMS FAITH” and “SMS MARIAM”) to provide offshore drilling services in March 2019.

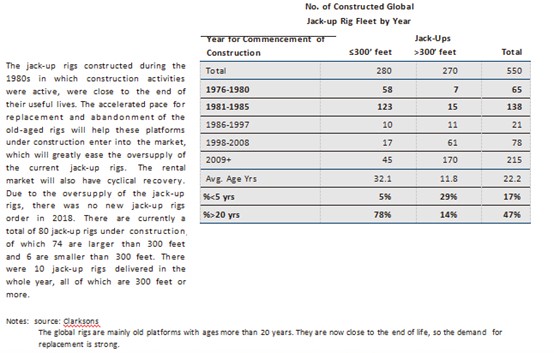

The global jack-up rig fleet is aging overall, and the demand for replacement is strong. Among the global jack-up rig fleets, 78% of the jack-up rigs with size smaller than 300 feet aged more than 20 years, and they are now close to the end of their useful lives. The demand for replacement is strong. Only 14% of the jack-up rigs with size larger than 300 feet aged more than 20 years and they are the main force of the current jack-up rig fleet.

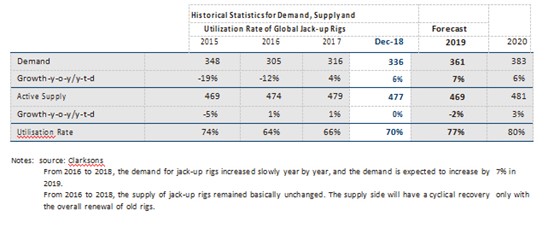

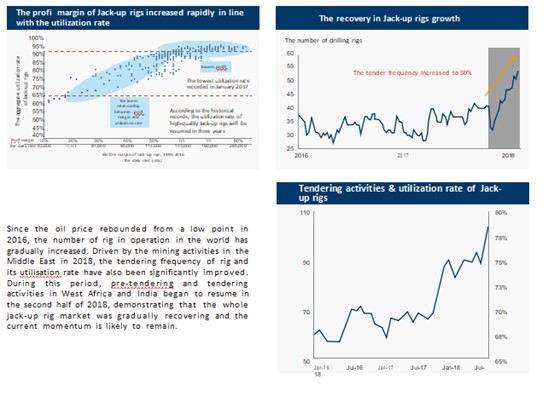

With the increase in the tender frequency of rigs of oil company, the utilisation rate and the daily rate of jack-up rigs rebounded. In 2018, the tender frequency of jack-up rigs increased by 83% from 30 rigs at the beginning of the year to 55 rigs. It is expected that the capital expenditure on offshore oil and gas E&P will increase by 9% in 2019. The utilisation rate of jack-up drilling rigs was around 65% in January 2017, the record low, reaching 70% by the end of 2018, and it is expected to reach 77% in 2019. The daily retirement and EBITDA margin will increase as the utilisation rate increased.

The graph on the right shows the pre-tendering and tendering activities of the jack-up rigs in different regions, calculated in terms of rigs per year. As shown in the graph, the Middle East market has recovered markedly since the beginning of 2017, while the activities of the rest of the world have increased significantly in the second half of 2018 after the launch of activities by international oil companies in West Africa and India.

According to statistics by Clarksons, as of the end of 2018, there were 79 cold stacked jack-up rigs and about 80 new jack-up rigs under construction in the world. Supply and demand will remain unbalanced in the next 1-2 years, and daily rent will be still low. However, owing to the sharp increase in the number of tenders offered by oil companies and the popularity of new high-specification platforms operating in shallow water, it is expected that platforms with high utilisation rate will be leased out first.

Large companies with strong cash flows in the industry have successively carried out M&A and integrations, while small companies were knocked out due to the exhaustion of the capital. The polarisation has become more apparent. In 2012, Shelf Drilling was established following the acquisition of 37 jack-up drilling rigs and 1 swamp barge from Transocean. Listed on the Oslo Bourse Norway in June 2018, Shelf Drilling is the world’s largest operator of jack-up rigs by number of active shallow water rigs and owns 38 rigs as at 31 December 2018, with a market capitalisation of around US$490 million.

The revenue of Shelf Drilling of US$613 million in 2018 increased by approximately US$41.0 million or approximately 7.2% as compared to US$572 million in 2017, mainly due to two new drilling rigs and three newly acquired rigs put into operation. At the same time, the average daily rate of rigs and utilisation rate were higher than the market average during the same period (sources: Shelf’s website).

Against the backdrop of merger and integration of the whole industry, CMIC managed to acquire shares in the world’s largest jack-up rig operator and successfully capture the high ground from the demand for global shallow-water jack-up rigs. Leveraging on the leading position of Shelf Drilling in the industry and its edges in superb operational management, the Company has entered the first echelon of global offshore asset operational management, which lays a solid foundation for the subsequent comprehensive development of offshore management business.

In 2019, CMIC would face opportunities and challenges while undergoing transformation and upgrade and exploring new business models. The Company will actively seize the timing when the global offshore market recovers from a prolonged downturn and to look for new opportunities. At present, CMIC adheres to a balanced development concept of “quality first, benefit priority, scale moderate” as the fundamental development strategy, focuses on “Offshore as the base, Energy as the value driver, Technology as the accelerator, Capital as the incubator and Globalization as the foundation”, and is committed to creating a “world class global marine energy technology industry chain value integration operator”. Appreciating that we operate in a dynamically changing global environment the Company will continually adapt in order to seize opportunities, optimise operations and to execute strategies to realise its long term vision. Based on its insight and grasp of the changing global industry, the Company would revise, optimise and continuously improve the ability to implement its strategies.